A LinkedIn post by SEBI-registered investment advisor Vivek S G (Sulegai) has sparked widespread discussion online after detailing how a Pune-based professional earning ₹90,000 a month slipped into a debt burden of ₹15 lakh following a family medical emergency.

The post by the founder of the financial advisory firm named Wealth Crafts has been liked a lot by people on the social media platform owing to its depiction of the gradual nature of financial emergencies.

A medical emergency led to the financial emergency

As per the post, the man in question had been living according to his means three years back.

Also Read | Before selling your ELSS, check if borrowing makes more sense

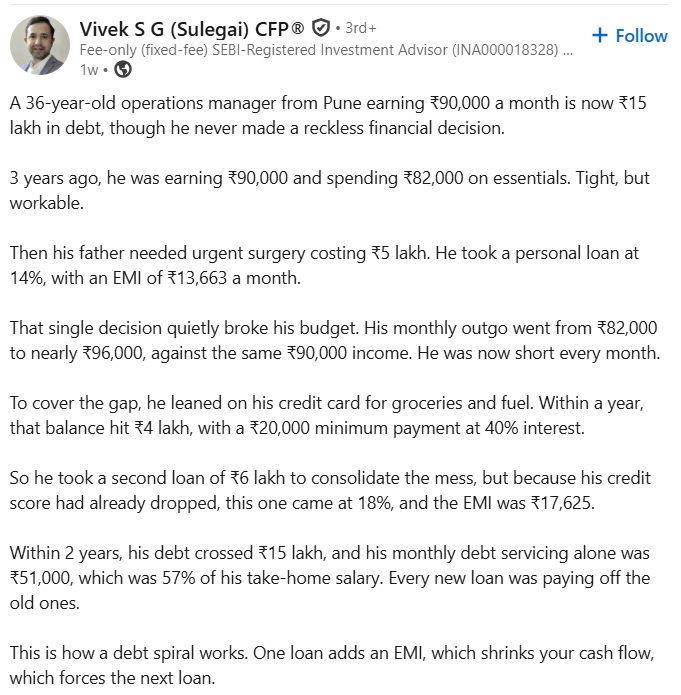

“A 36-year-old operations manager from Pune earning ₹90,000 a month is now ₹15 lakh in debt, though he never made a reckless financial decision,” Vivek wrote in his post.

The financial advisor explained that the man used to earn ₹90,000 per month while spending around ₹82,000 in his expenses.

“Three years ago, he was earning ₹90,000 and spending ₹82,000 on essentials. Tight, but workable,” Vivek wrote.

The turning point came when the man’s father required urgent surgery costing ₹5 lakh.

“He took a personal loan at 14%, with an EMI of ₹13,663 a month,” Vivek stated.

According to the advisor, the additional monthly repayment pushed the family’s expenses beyond its income, creating a persistent monthly shortfall.

How the debt spiral grew

To bridge the gap between income and expenses, the individual reportedly began using credit cards for routine expenses such as groceries and fuel.

According to Vivek, the outstanding credit card balance reached ₹4 lakh within a year.

“To cover the gap, he leaned on his credit card for groceries and fuel. Within a year, that balance hit ₹4 lakh, with a ₹20,000 minimum payment at 40% interest,” he wrote.

Attempting to manage the growing debt, the individual then reportedly took a second loan of ₹6 lakh. However, by then, his credit score had deteriorated, resulting in a higher interest rate.

“He took a second loan of ₹6 lakh to consolidate the mess, but because his credit score had already dropped, this one came at 18%,” Vivek wrote.

The advisor said the debt burden eventually crossed ₹15 lakh, with monthly repayments alone consuming more than half of the individual’s take-home salary.

“This is how a debt spiral works. One loan adds an EMI, which shrinks your cash flow, which forces the next loan,” he explained.

Warning signs borrowers should watch for

According to Vivek, three major factors typically accelerate debt

spirals:

Credit card interest rates of 35-40%

Late payment penalties

Falling credit scores leading to more expensive borrowing

He advised borrowers to treat monthly EMIs exceeding 40% of take-home income as a warning sign.

Also Read | Noida International Airport expands network with direct flights to 16 cities across India

“If your monthly EMIs are already above 40% of your take-home, treat it as a warning,” he wrote.

The financial advisor recommended avoiding fresh loans, preparing a list of all liabilities and prioritising repayment of the highest-interest debt first.

Social media users say story reflects reality

The post attracted significant engagement on LinkedIn, with many users saying the story highlighted how financial distress often develops slowly.

One user commented:

“Debt spirals rarely begin with bad decisions. They often begin with life happening at the worst possible time, and not having enough margin to absorb it.”

Another said:

“I always advise people to save for emergencies beforehand. It is much better than borrowing money later.”

Some mentioned that in most cases, the problem lies in making several poor decisions under pressure.

Viral posts have once again initiated discussions about the necessity of saving for emergencies, insuring, and proper financial planning during unexpected events.

FAQs

What is the reason behind the ₹15 lakh debt of the Pune professional?

According to the viral LinkedIn post, a family emergency led to the person taking a personal loan, after which he took loans using credit cards.

What is considered a warning sign of a debt spiral?

Financial advisor Vivek S G said monthly EMIs exceeding 40% of take-home income should be treated as an early warning sign of financial distress.

{News Ei Samay does not provide investment advice anywhere. Investment and trading in the share market or any field involve risk. Proper study and expert advice are recommended beforehand. This news is published for educational and awareness purposes.}